An Evolutionary Macroeconomic Perspective on Australia's Current Economic Malaise

Bipartisan creativity and cooperation is needed urgently!

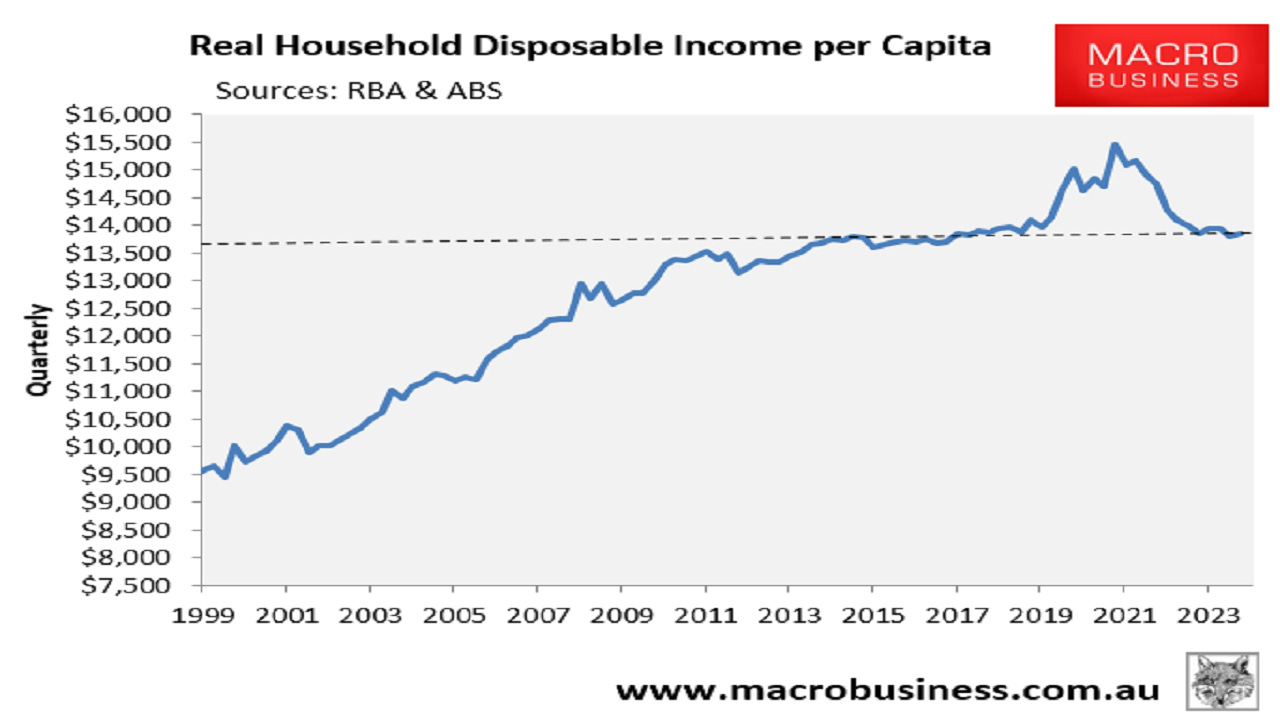

There has been much discussion in the press concerning the recent reductions in both GDP per capita and disposable income per capita. Although we are technically not in a recession yet, mainly thanks to population growth, it is argued by many that these two negatives are recessionary features. If we look at the recent Macro Business Chart below, we can see that these negative tendencies are just the unwinding of excessively high disposable income per capita because of large subsidies in the COVID period. Australia has returned to where it was in 2019. In other words, ignoring the COVID effect, disposable income per capita has actually exhibited no growth for a decade. So, Australia’s current malaise seems to be due to longer term factors than the recent machinations of monetary and fiscal policies that we read about daily in the media.

In 2016, I published an article on the “Australian Growth Miracle” modelling Australian economic growth over the period 1904-2008.1 The methodology used was ‘augmented logistic diffusion modelling’ (ALDM). This is an evolutionary macroeconomic econometric methodology that sees economic growth as following successive long term logistic (slanty S-shaped) diffusion processes, driven by the emergence of radical organizational and/or technological innovations which open up a growth niche which is entered via capital investments.

It was discovered that there is evidence in support of the hypothesis that Australia has followed two distinct long term logistic diffusion paths over the chosen period. One from 2004 to 1938, and, after the Second World War, a second from 1948-2008. The conclusion of the article was optimistic, with an estimate that, in 2008, because of past capital investments, Australian real GDP was still 24% away from its logistic limit. This was unlike, for example, the UK, where a previous study of mine found it to be close to its logistic limit. Thus, the label “miracle” for Australia. Through robust private and public sector investment, and largely bipartisan policymaking and regulatory changes, Australia had escaped the limit it had previously reached by the commencement of the Second World War.

I have not updated this study, but there is casual evidence that Australia seems to have progressed quite rapidly into the slowdown period of a logistic growth path. Since the end of my data set, 2008, capital investment has weakened significantly for a range of reasons. In other words, in sixteen years, Australia seems to have moved much closer to a logistic growth limit. Real household disposable income per capita, as illustrated in Macro Business’s Chart, seems to have already reached its limit quite a decade ago.

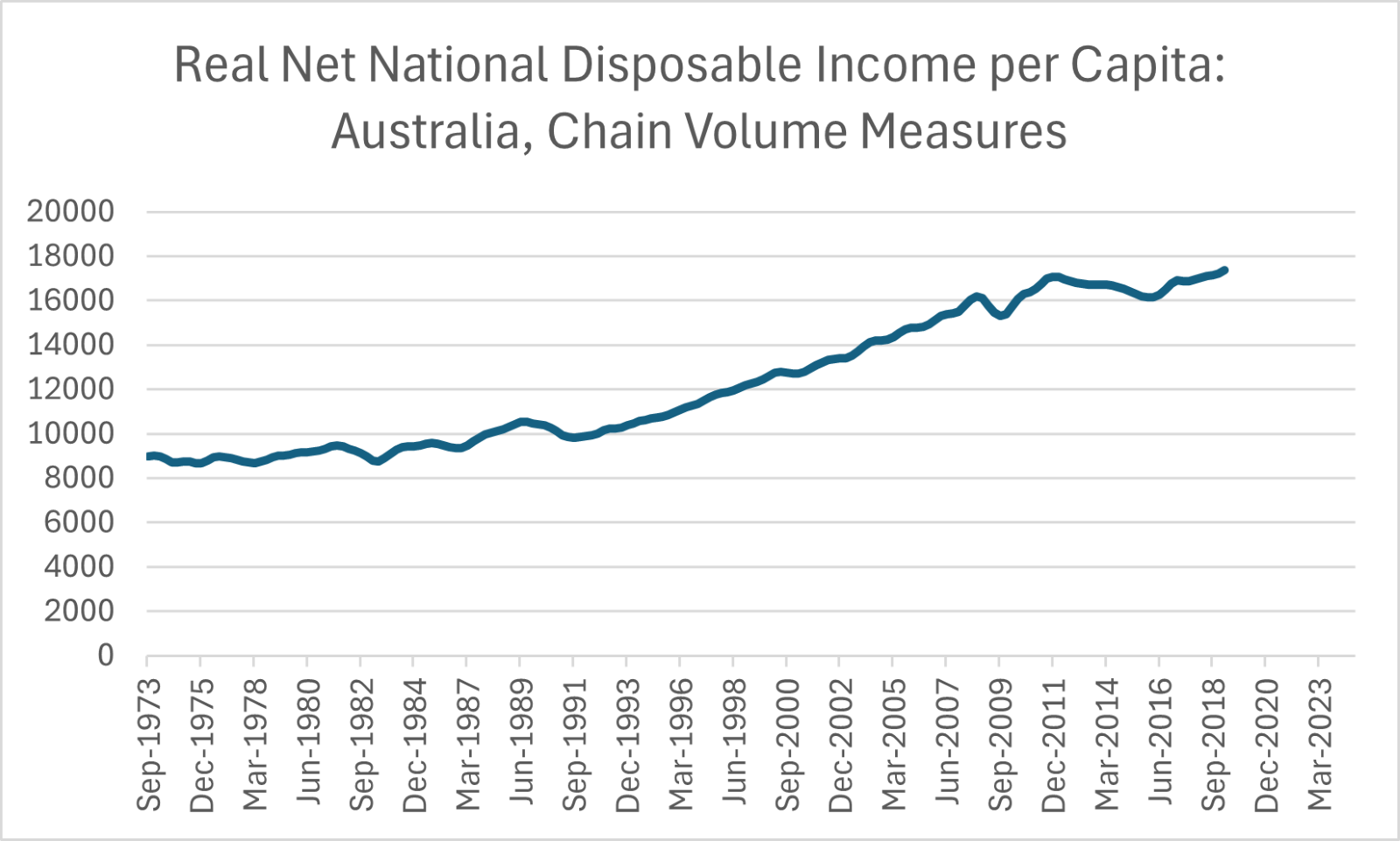

If we use a closely related, seasonally adjusted, ABS series available from 1973 to 2019, we can see a logistic path clearly, with an inflexion phase around 2000. After a COVID induced a temporary burst of disposable income growth, stasis had resumed by the end of 2022.

In my ‘growth miracle’ article, there was evidence of a temporary reversal in the 1970s of the postwar tendency for the estimated niche limit to rise faster than real GDP, before recovering again in the 1980s. Capital investment is the key driver of a logistic niche limit on growth in these models, and it stagnated in the 1970s. Real disposable income is, of course, not the same as real GDP. They vary depending mainly on taxation and subsidies. In recessionary conditions, such as those in the 1970s, government spending rose strongly as part of stabilization policy in the face of declines in business investment. The goal was to stop real disposable income per capita from falling and this was done by increasing the budget deficit. GDP growth was negative but real disposable income per capita held up.

This policy-induced flattening out of disposable income per capita means that it is higher than otherwise, so a shorter logistic for disposable income emerges between significant slowdowns that occur on the long-term logistic growth path. There are also policy induced blips on this trend. For example, in 2008-9 stabilization policy, to deal with a macroeconomic shock emanating from the US, was so strong that recession was actually averted and real disposable income per capita increased temporarily, well above its trend. Again, when COVID hit, the priority was maintenance of disposable income in the face of a shock. This was severely overdone by Federal and State governments, producing household surpluses in the face of severe domestic and international supply contractions. This was an imbalance that would go on to generate inflation, as it did in many other countries.

The problem with all these laudable efforts to stop significant drops in disposable income is that it blurs the longer-term picture and leads to an over-preoccupation with short-term developments. So, all the discussions about short-term policy and the associated blame games are misplaced. What we are facing is a medium to long-term evolutionary economic problem which has emerged while both major parties have been in government. Evolutionary economics tells us that, when a logistic growth limit is reached because of the weakening of business investment as entrepreneurial opportunities dry up, there must be radical organizational and/or technological innovation, otherwise economic decline and all of its political consequences will intensify.

Static real disposable income per capita and associated static real consumption per capita, particularly given that there must be inequality of impact, makes a significant part of the population disillusioned and restless. The data we have is about averages. But there is a distribution of experiences above and below. Those above tend to be high income recipients and those below the opposite. This matters much more when growth of disposable income has slowed to zero. We need only look over to the US to appreciate the impact of systemic inequality. Despite continuing economic growth there, real consumption has been static or in decline for a large proportion of the population. And we are seeing the political consequences.

There are no easy answers when it comes to designing policies to induce investments in radical innovations, especially when stasis has caused political polarization to intensify reducing the probability of bipartisanship. But what is certain is that short term political squabbles have to be set aside, as they have been in the past, in favour of bipartisan debate and cooperation concerning the applicability of new strategies and policies. And big questions, before we get to discussing the details of possible medium- and long-term policies, are: what kind of economic growth, if any, is sustainable in the long run, and how should income yielded by our collective economic activities be distributed?

Foster, John (2016), “The Australian growth miracle: an evolutionary macroeconomic explanation,” Cambridge Journal of Economics, Volume 40, Issue 3, Pages 871–894.